Benchmarks of Global Clean Energy Manufacturing assesses manufacturing supply chains for four leading clean energy technologies: crystalline silicon solar PV modules, LED packages, wind turbine components, and lithium-ion batteries. Photos courtesy of iStock

February 12, 2021—As clean energy manufacturing becomes a greater share of the global economy, manufacturers and decision makers are seeking opportunities in the manufacture, sale, and installation of clean energy technologies.

To help inform manufacturing and policy decisions, the Clean Energy Manufacturing Analysis Center (CEMAC), a key program under the umbrella of the Joint Institute for Strategic Energy Analysis (JISEA), has released an updated version of its

Benchmarks of Global Clean Energy Manufacturing report through the support of the U.S. Department of Energy's Office of Energy Efficiency and Renewable Energy.

The report assesses technologies in terms of

common points of reference, or benchmarks, including market characteristics, global trade flows, and manufacturing value added. Although many organizations have analyzed market aspects of clean energy manufacturing, trade and value added are unique to this report. These benchmarks provide insight into the shifting clean energy manufacturing landscape between 2014 and 2016 to help guide research agendas, highlight trade impacts, and identify manufacturing opportunities by location and technology.

Building on the first

Benchmarks report, the latest version assesses manufacturing of four leading clean energy technologies—wind turbine components, crystalline silicon solar photovoltaic (PV) modules, vehicle lithium-ion battery (LIB) cells, and light-emitting diode (LED) packages—in 13 economies over 3 years from 2014 to 2016.

"CEMAC's updated report, Benchmarks of Global Clean Energy Manufacturing, makes economic data on clean energy technologies widely available," said Jill Engel-Cox, JISEA Director, "and the report supports deeper insights into balance of trade effects on upstream materials."

Crosscutting Findings

With the highest production of the four benchmarked clean energy technologies, China played the largest role in supporting global demand for these technologies from 2014 to 2016. In addition, China was the only benchmarked economy that had sufficient production to meet domestic demand for the four clean technology end products (although not for all the supply chain intermediates considered).

Gaps between production and demand across the economies and the supply chain were met through an extensive global trade network. From 2014 to 2016, aggregate exports (when measured in U.S. dollars) for the 13 economies declined 7.3% from $39.5 billion to $36.6 billion, while imports declined 9.2% from $51 billion to $46.3 billion. China was the largest exporter of benchmark technologies and the United States was the largest net importer.

The total value added from production of the four benchmark technologies across the 13 economies increased from $89.6 billion in 2014 to $102.4 billion in 2015 and then dropped to $87.3 billion in 2016, in part due to declining unit costs of clean energy technologies. China accrued the largest total value added from manufacturing the four clean energy end products analyzed, amassing three to four times more than each of the following three economies (the United States, Japan, and Germany).

All the analyzed economies accrued indirect value added from the global production of intermediate material, subcomponents, and services related to end product manufacturing of the four technologies in other economies. China was the largest supplier of these intermediates to all the other countries, contributing the most indirect value added to the other benchmarked economies.

Still, the greatest share of total value added to the benchmarked economies over the period generally came from domestic production of the technologies, primarily processing materials, manufacturing components, and providing services throughout the supply chain (indirect value added) rather than assembling the clean energy technology end products themselves (direct value added).

Wind Turbines

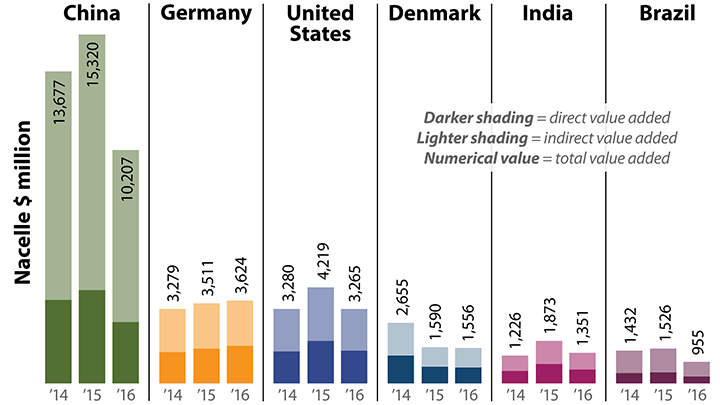

Wind Turbine Supply Chain Value Added, 2014–2016

Analysts assessed total value added, indirect value added, and direct value added to each benchmarked economy across the wind turbine supply chain by individual technology component. As shown for nacelles here, indirect value added was also higher than direct value added across the supply chain, except for towers in Denmark and blades in China.

Download chartWind turbine component prices declined from 2014 to 2016—the average installed wind costs decreased by 8% globally and 7% in the United States. Despite the price declines through 2016, wind turbines remained the most capital-intensive of the technology end products evaluated over the period. Economies derived greater value added from manufacturing components than from other clean energy technology intermediates.

Between 2014-2016, wind energy technology demand, production, trade flows, and value added was highest in 2015 with uncertainty around the renewal of the U.S. renewable electricity production tax credit.

China, Germany, and the United States accrued more total value added from manufacturing wind turbine components from 2014 to 2016 than other benchmarked economies over the period. Generally, indirect value added was greater than direct value added across the wind turbine supply chain, except for towers in Denmark and blades in China.

Key drivers of wind turbine supply chain trends over the period included:

- Declining wind turbine component prices resulting from maturing supply chains

- Expiration and reduction of subsidies to promote wind turbine manufacturing and deployment

- Preference for domestic production due to cost and logistic challenges associated with transporting large wind turbine components.

Crystalline Silicon PV Modules

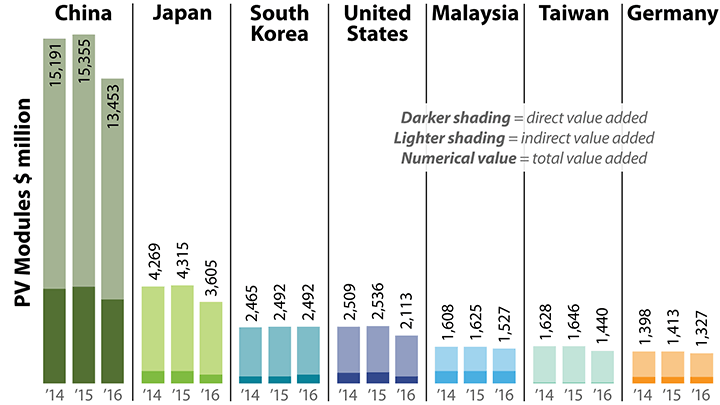

PV Module Supply Chain Value Added, 2014–2016

Analysts assessed total value added, indirect value added, and direct value added to each benchmarked economy across the PV module supply chain by individual component. The total value added from global production of PV modules generally declined over the period, with indirect value added generally greater than direct value added. Download chart

Demand increased for PV modules from 2014 to 2016, driven in part by domestic policies that set targets for renewable deployment or provided incentives to offset costs. Global manufacturing capacity expanded to meet the demand, resulting in excess capacity and contributing to significant declines in prices over the period, including prices for residential- and utility-scale system components.

China maintained its position with the highest demand, production, and manufacturing capacity of the benchmarked economies and contributed indirect value added to the other economies. Policies and equipment contracting approaches like installation targets or tax credits helped stimulate PV Chinese markets.

In the benchmarked economies, the balance of trade (exports minus imports) remained relatively stable across the PV module supply chain, with a few exceptions including PV modules in Japan and the United States, PV cells in China and Taiwan, and polysilicon in Taiwan. Some net importers of end products, such as the United States, were also major exporters of upstream processed materials and/or subcomponents for the same technologies, illustrating the complexity of clean technology manufacturing and trade.

Key drivers of PV module supply chain trends over the period included:

- Declining cost of solar projects driven by manufacturing capacity increases, manufacturing cost reductions, module efficiency improvements, and module and supply chain intermediate surpluses in the global market

- Global demand growth driven, in part, by declining prices and improved module efficiencies

- Shifting markets that stimulate policies and equipment contracting approaches, including installation targets, tax credits, auctions, and targeted tariffs

LED Packages

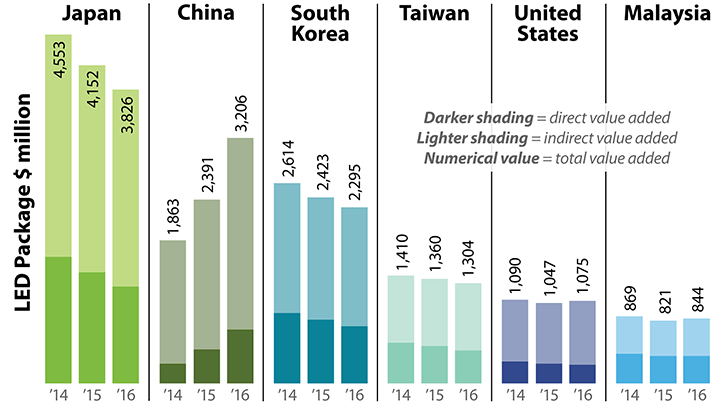

LED Package Supply Chain Value Added, 2014–2016

Analysts assessed total value added, indirect value added, and direct value added to each benchmarked economy across the LED package supply chain by component. The total value added from the production of LED packages in benchmarked economies was up slightly, from $13 billion in 2014 to $13.2 billion in 2016.

Download chart

LED packages are used in manufacturing lighting and electronics. Global demand for LED packages, chips, and sapphire substrate grew rapidly between 2014 and 2016, led by China. Demand in other benchmarked economies was relatively flat. Only Taiwan had sufficient domestic production to meet its demand across the supply chain; other economies relied on trade to fill supply chain gaps.

Between 2014 and 2016, annual global production and demand for LED packages increased by 37.8%. The most significant increases were seen in China, where many new foundries came online in 2015. This abruptly reduced imports from Taiwan, contributing to a sharp reduction in China's net imports and Taiwan's net exports from 2015 to 2016.

Of the benchmarked economies, total value added from global production of LED packages, chips, and sapphire substrate was greatest for Japan, China, South Korea, and Taiwan. Indirect value added was greater than direct value added for all LED supply chain intermediates considered. Except for China, direct value added from domestic production of LED packages declined or remained steady for all economies from 2014 to 2016.

Key drivers of LED package supply chain trends over the period included:

- Growth in demand related to regulated phaseouts of incandescent lighting

- Declining prices from oversupply and industry consolidation.

Lithium-Ion Battery Cells for Light-Duty Electric Vehicles

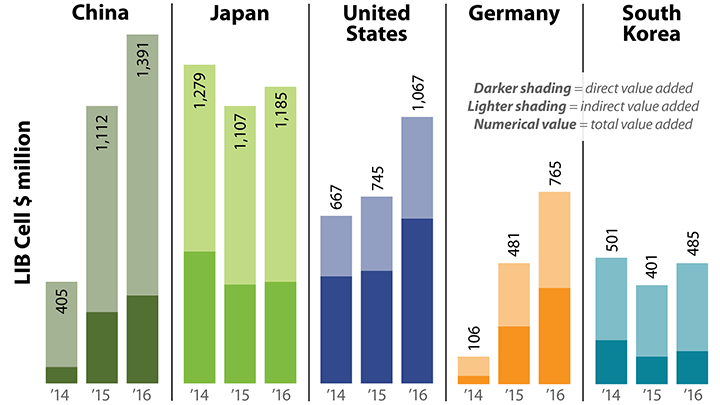

Vehicle Lithium-Ion Battery Cell Supply Chain Value Added, 2014–2016

Analysts assessed total value added, indirect value added, and direct value added to benchmarked economies across the lithium-ion battery cell supply chain by individual technology component. The total value added from lithium-ion battery cells increased the most in Germany, China, and the United States from 2014 to 2016, as production ramped up to meet growing electric vehicle demand in those economies. Download chart

Demand for lithium-ion battery cells grew significantly from 2014 to 2016, driven by investment in electric vehicles (EVs). Global manufacturing capacity soared in 2016 in anticipation of continued investment in EVs, creating excess capacity across the supply chain intermediates.

China, Japan, and South Korea were top producers of technology intermediates and were top net exporters of lithium-ion battery cells. Although the United States and Germany were leaders in electric vehicle deployment, they were top net importers of lithium-ion battery cells because of limited domestic supply chains. Japan produced more lithium-ion battery cells than its domestic market demand and exported to other countries in North America and Europe.

Total value added from lithium-ion battery cells increased the most in Germany, China, and the United States over the period. Indirect value added was greater than direct value added across the entire supply chain for all lithium-ion battery intermediates and economies considered, except for cells in the United States.

Key drivers of LIB cell supply chain trends over the period included:

- Growing global demand for LIB cells in the manufacture of battery packs used in electric vehicles

- Development and expansion of domestic LIB cell manufacturing supply chains to meet all or part of domestic demand growth

- China's strong backing of its domestic LIB industry through policy and investment to support deployment of electric vehicles.

Learn More

Learn more about the framework analysis in this report and access additional resources for CEMAC's benchmarks of global clean energy manufacturing, including interactive trade chord charts. Get the high-level findings in our JISEA Research Highlight.