Geothermal Power Plant Turbines: First Look at the Manufacturing Value Chain

June 3, 2016 — The global geothermal market has significantly grown over the last decade. In the 10 years ending in December 2015, 118 binary cycle, 58 flash cycle and 14 dry steam geothermal power plants were installed around the world, including (in order of installed capacity) the United States, New Zealand, Turkey, Indonesia, Kenya, Iceland, Italy, Mexico, Nicaragua, Philippines, Germany, El Salvador, Papua New Guinea, Costa Rica, Guatemala, Japan, Portugal, China, Russia, France, Australia, Romania and Taiwan. The additions increased global geothermal power capacity by 4.4 GW to 13.3 GW.

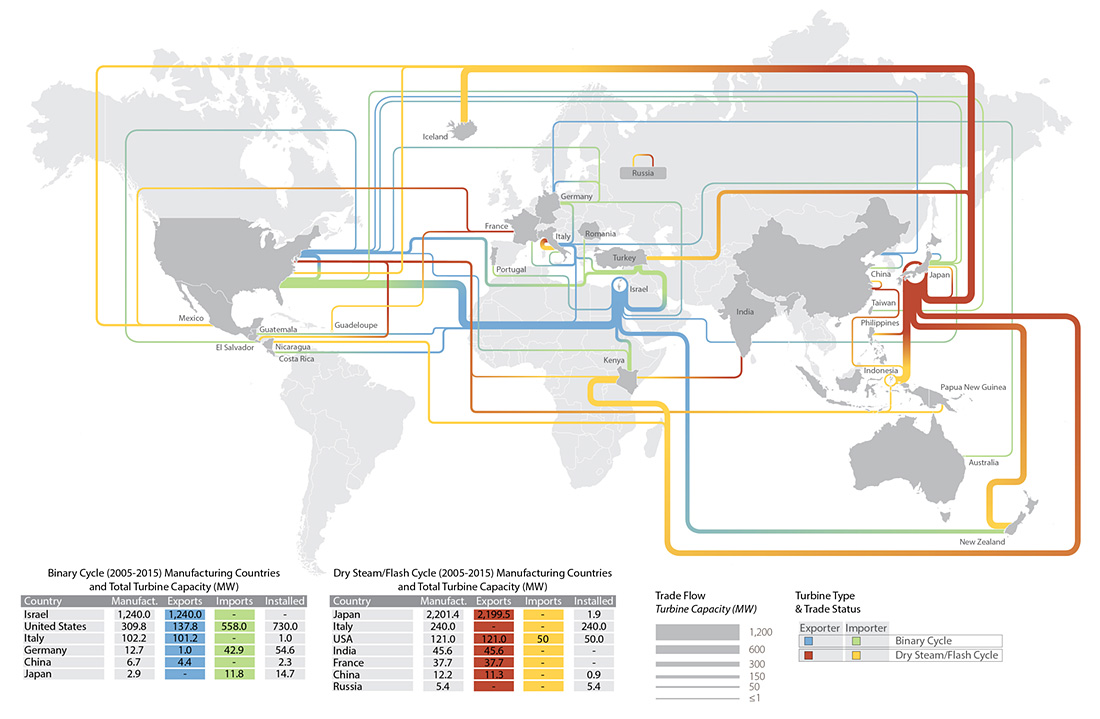

Although the new power plants were mostly binary cycle, the greatest share of new capacity (49.5%) was in flash cycle plants. The capacity share of binary cycle and dry steam turbines was 38.7% and 11.8% respectively.

Binary cycle turbine manufacturing is dominated by Israel followed by the United States, Italy, and Germany. The flash cycle and dry steam turbine manufacturing is dominated by Japan followed by Italy, the United States, France, Russia, and China. The attached map shows global trade in these two technology types.

The market for geothermal technology is expected to continue growing and reach about 18.4 GW by 2021. Based on developing projects and forecasts, there will be high demand for a diverse mix of geothermal turbine types from Europe and the United States, East Africa, South East Asia and the South Pacific.

These results are the early findings of our CEMAC study on the manufacturing value chain of geothermal power plant turbines. Watch for more robust insights on the manufacturing value chain of geothermal power plant turbines later in 2016.

Back to JISEA News >